Save up to 20% today!

Legal, Financial & Planning Resources

Preparing for a Secure and Dignified Future

FINANCE

2/6/20264 min read

Legal, Financial & Planning Resources

Preparing for a Secure and Dignified Future

Planning for the later stages of life is one of the most important — and often most overwhelming — responsibilities for seniors and their families. Legal documents, healthcare decisions, insurance options, and long-term care planning can feel complex, emotional, and confusing without the right guidance.

At ElderlyCareInfo.com, we aim to simplify these topics so families can make confident, informed choices. Below are essential legal, financial, and care-planning resources every aging adult and caregiver should understand.

Essential Legal Documents for Aging Adults

Having proper legal documents in place ensures your wishes are respected if illness, injury, or cognitive decline occurs.

Advance Directives

Advance directives outline healthcare decisions if someone cannot speak for themselves. These often include:

Living Will – Specifies medical treatment preferences.

Healthcare Proxy – Names a person to make medical decisions on your behalf.

These documents protect both the senior and the family from uncertainty during emergencies.

Power of Attorney (POA)

A power of attorney authorizes a trusted person to handle financial or legal matters if the senior becomes unable to do so.

Types include:

Financial POA – Manages bills, assets, and accounts.

Healthcare POA – Makes medical decisions when needed.

Creating these documents early prevents costly court involvement and family conflict later.

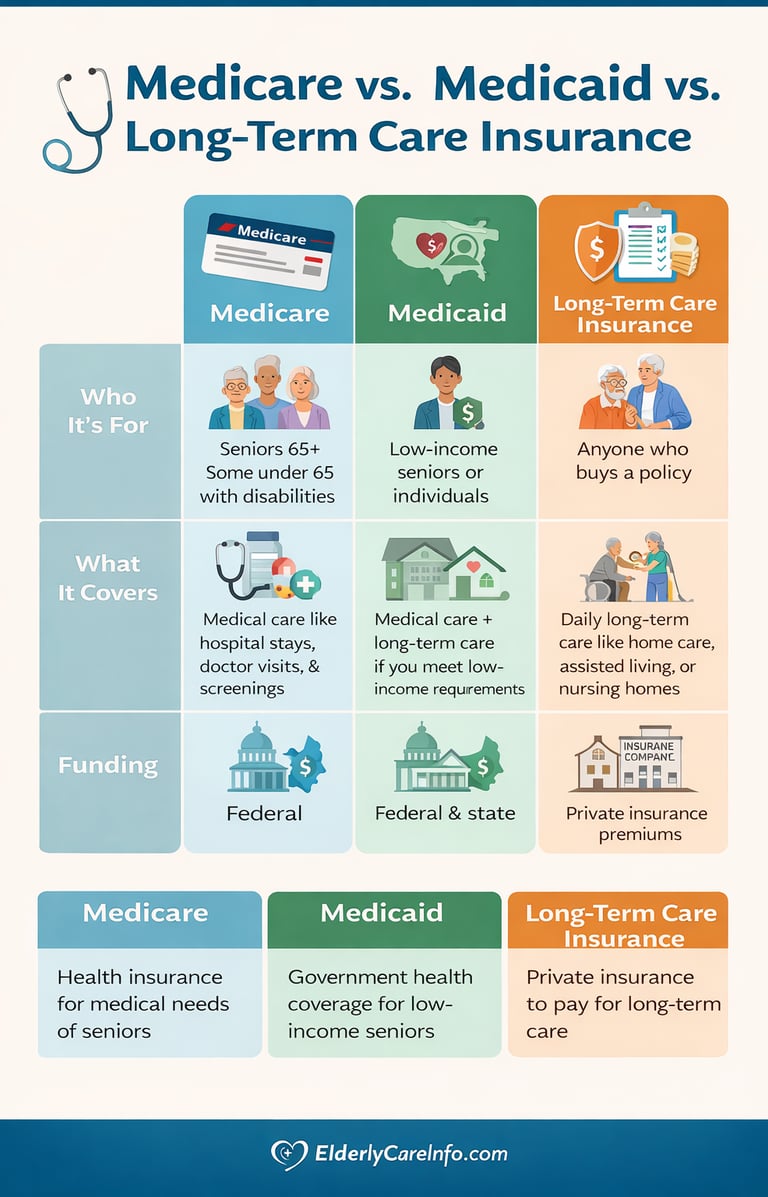

Understanding Medicare, Medicaid, and Long-Term Care Insurance

Navigating healthcare and long-term care options can feel overwhelming for seniors and their families, but understanding the basics is the first step toward making informed decisions. Medicare is a federal health insurance program primarily for adults 65 and older, covering hospital stays, doctor visits, and preventive care. While it provides essential medical coverage, it generally does not cover long-term custodial care, such as help with bathing, dressing, or daily activities.

In contrast, Medicaid is a joint federal and state program that offers health coverage for low-income individuals, including seniors. It can cover long-term care services at home or in nursing facilities, but eligibility depends on income and assets, which vary by state. Long-Term Care (LTC) Insurance is a private option designed specifically to cover the costs of daily assistance and custodial care, whether at home, in assisted living, or in a nursing facility. Understanding how these programs differ helps families plan for both medical needs and long-term care while maintaining financial and personal security.

Medicare

Medicare applications are primarily handled by the Social Security Administration (SSA) online at ssa.gov, by phone at 1-800-772-1213.

Medicare generally covers:

Hospital stays

Doctor visits

Preventive services

However, it usually does not cover long-term custodial care, such as daily assistance with bathing or toileting.

What it is: A federal health insurance program primarily for people 65 and older, and for some younger individuals with disabilities.

Coverage:

Hospital care (Part A)

Medical services like doctor visits (Part B)

Optional private plans (Part C/Medicare Advantage)

Prescription drugs (Part D)

What it doesn’t cover: Most long-term custodial care (help with bathing, toileting, dressing), most dental, hearing, or vision care.

Who pays: Funded through federal payroll taxes, premiums, and co-pays.

Medicaid

Applying for Medicaid in the United States can be done several different ways, depending on what is most convenient for you. Most people choose to apply online through their state’s Medicaid program, which is typically the quickest option. You can start by visiting Medicaid.gov, where you’ll be directed to your state’s official application site.

Another option is to apply through the federal Health Insurance Marketplace at HealthCare.gov. When you submit an application there, your information is securely forwarded to your state Medicaid office to determine eligibility.

Medicaid helps pay for long-term care for individuals with limited income and assets. It often covers:

Nursing home care

Some in-home services

Assisted living in certain states

Eligibility varies by state and financial situation.

What it is: A joint federal and state program that provides health coverage for people with low income and limited assets, including seniors.

Coverage:

Can cover long-term care in nursing homes or some home care services

Doctor visits, hospital care, prescriptions, and preventive care

Eligibility: Means-tested (depends on income and assets), and rules vary by state.

Who pays: Funded by both federal and state governments.

Long-Term Care Insurance

This private insurance helps cover costs for:

Home care

Assisted living

Memory care

Nursing facilities

Policies differ, so reviewing coverage early — before health issues arise — can save significant money later.

Understanding the differences between these programs helps families avoid surprises and plan responsibly.

What it is: A private insurance policy that helps pay for long-term custodial care, usually not covered by Medicare.

Coverage:

Assistance with activities of daily living (ADLs) like bathing, dressing, eating, and mobility

Home care, assisted living, or nursing home stays depending on the policy

Eligibility: You must purchase a policy in advance, typically before serious health issues arise.

Who pays: You pay premiums to the insurance company; benefits are triggered when you meet the policy’s conditions (like needing help with ADLs).

LTC insurance is private coverage designed to help pay for extended daily care, whether at home, assisted living, or a nursing facility.

Financial Planning Tips for Retirement and Care Costs

Long-term care can be one of the largest expenses families face.

Helpful financial planning steps include:

Create a care budget including housing, healthcare, medications, and assistance services.

Review income sources such as Social Security, pensions, and investments.

Protect assets legally with estate planning and elder-law guidance.

Plan for inflation and medical cost increases.

Avoid last-minute decisions by preparing while the senior is still healthy.

Consulting a financial advisor or elder-law attorney can help align financial resources with realistic care expectations.

How to Choose Between Assisted Living, Home Care, and Memory Care

Selecting the right care environment depends on health, safety, and personal preferences.

Home Care

Best for seniors who:

Want to stay in their own home

Need help with daily tasks

Are medically stable

Home care supports independence and comfort with minimal disruption.

Assisted Living

Ideal for seniors who:

Need help with medications, meals, and activities

Want social interaction

Are mostly independent but need supervision

Assisted living offers structure without full medical care.

Memory Care

Designed for seniors with:

Alzheimer’s disease

Dementia

Cognitive decline

These communities provide specialized safety, routines, and trained staff for cognitive health.

The right choice balances safety, dignity, budget, and quality of life.

Planning Today Protects Tomorrow

Legal, financial, and care planning are not just paperwork — they are acts of protection, clarity, and love for aging adults and their families.

By preparing advance directives, understanding healthcare programs, planning finances, and choosing the right care environment, families reduce stress and avoid crisis decisions.

At ElderlyCareInfo.com, we support informed, compassionate planning so seniors can age with security, dignity, and peace of mind.

Elderly Care Info

Reliable information and practical solutions for dignified senior care.

Contact

Newsletter

info@elderlycareinfo.com

© 2026. All rights reserved.