Save up to 20% today!

Social Security Claiming Strategies

Maximizing Benefits Through Smart Timing, Spousal Options and Long-Term Planning

FINANCE

2/27/20262 min read

Social Security Claiming Strategies

How to Maximize Your Benefits Through Smart Timing, Spousal Options, and Long-Term Planning

When it comes to retirement income planning, few decisions carry as much long-term impact as when and how you claim Social Security benefits. A thoughtful claiming strategy can mean tens of thousands of dollars in additional lifetime income, while a rushed decision may permanently reduce your monthly benefit. Understanding the rules, timelines, and optimization tactics is essential.

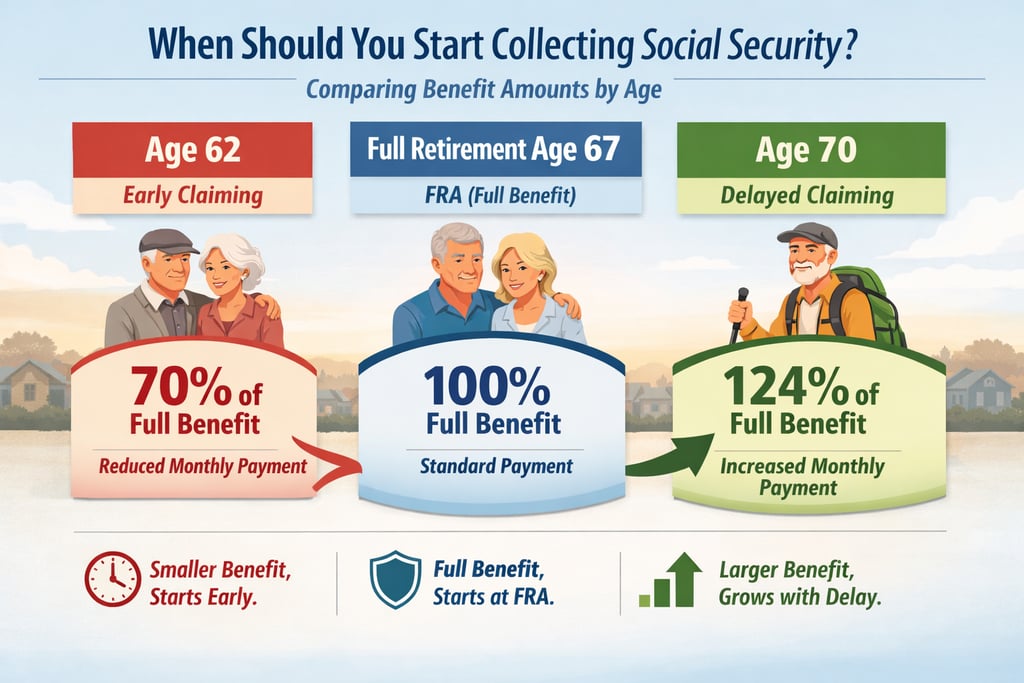

Understanding Your Full Retirement Age (FRA)

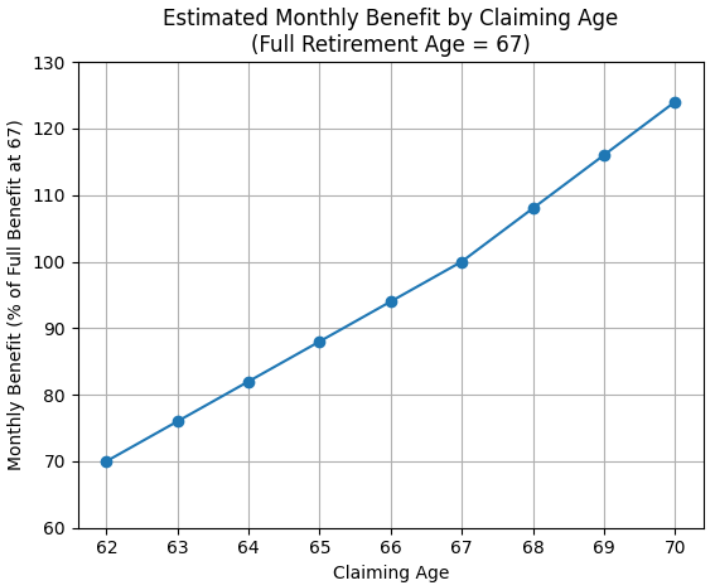

Your Full Retirement Age (FRA) is the age at which you are eligible to receive 100% of your earned Social Security benefit. FRA varies based on your birth year, typically ranging from 66 to 67.

Claim at 62 (early): Benefits are permanently reduced (up to 30% lower than FRA benefits).

Claim at FRA: You receive your full primary insurance amount (PIA).

Delay until 70: Benefits increase by approximately 8% per year past FRA due to delayed retirement credits.

For individuals in good health with longevity in their family history, delaying benefits can significantly increase lifetime income, particularly if you live into your 80s or 90s.

Spousal and Survivor Strategies

Married couples have additional planning opportunities:

Spousal benefits: A spouse may claim up to 50% of the higher earner’s FRA benefit.

Survivor benefits: Upon the death of one spouse, the surviving spouse may receive the higher of the two benefits.

Strategic sequencing: Often, the lower-earning spouse claims earlier while the higher earner delays to maximize the survivor benefit.

These decisions can substantially impact household lifetime income and the financial stability of the surviving spouse.

Working While Claiming Benefits

If you claim benefits before FRA and continue working, the Social Security earnings test may temporarily reduce your benefits if you exceed annual income limits. Once you reach FRA, these reductions cease, and your benefit is recalculated.

For individuals planning part-time work in early retirement, timing claims carefully can prevent unnecessary reductions.

Tax Considerations

Up to 85% of Social Security benefits may be taxable depending on your combined income (including pensions, IRA withdrawals, and investment income). Coordinating withdrawals from retirement accounts with Social Security timing can help manage tax brackets and preserve after-tax income.

Strategic tax planning in the years between retirement and age 70 can improve overall retirement sustainability.

Coordinating Social Security With Your Broader Retirement Plan

Social Security should not be evaluated in isolation. It interacts with:

Required Minimum Distributions (RMDs)

Pension income

Investment withdrawal strategies

Healthcare costs and Medicare premiums

Longevity risk management

For many retirees, delaying Social Security acts as a form of inflation-adjusted longevity insurance, reducing pressure on investment portfolios later in life.

Conclusion

There is no universal “best” age to claim Social Security. The optimal strategy depends on health, marital status, work plans, financial assets, and risk tolerance. A disciplined evaluation of timing, spousal coordination, and tax implications can materially enhance retirement income security.

Before filing, consider running multiple scenarios or consulting with a retirement income specialist to ensure your claiming strategy aligns with your long-term financial objectives.

Break-Even Analysis: When Does Delaying Pay Off?

A core concept in Social Security strategy is the “break-even age.” This is the age at which total lifetime benefits from delaying equal the amount you would have received by claiming early.

For many retirees, the break-even point falls around age 78–82. If you expect to live beyond that range, delaying may be financially advantageous. However, personal health, need for income, and portfolio strength all matter.

Elderly Care Info

Reliable information and practical solutions for dignified senior care.

Contact

Newsletter

info@elderlycareinfo.com

© 2026. All rights reserved.